📖 Start SIP with ₹500: My Honest Beginner Journey

Not long ago, I was sitting on ₹500 in my bank account, unsure whether to save it, spend it, or just let it sit.

Everywhere I looked, people were shouting about SIPs, mutual funds, compounding, and how I was “losing money by not investing.”

But no one was answering the one question I had:

“Can I really start SIP with ₹500? And if yes… how?”

The answer turned out to be YES — and today, I want to walk you through everything I learned.

This post isn’t a lecture.

It’s a beginner’s blueprint — from someone who decided to start SIP with ₹500 and is now growing slow but steady.

🧠 What Is SIP? (Explained Like I’m 5)

Let’s kill the jargon first.

SIP = Systematic Investment Plan

Which means: You invest a fixed amount — like ₹500 — every month into a mutual fund. That fund invests in stocks or bonds for you.

Think of it like an EMI — but instead of paying for a phone, you’re paying into your future.

So when you start SIP with ₹500, you’re sending your money on a long-term mission — to grow.

💸 How I Actually Started SIP with ₹500

I didn’t have fancy tools, advisors, or financial training.

I had Instagram ads and Google.

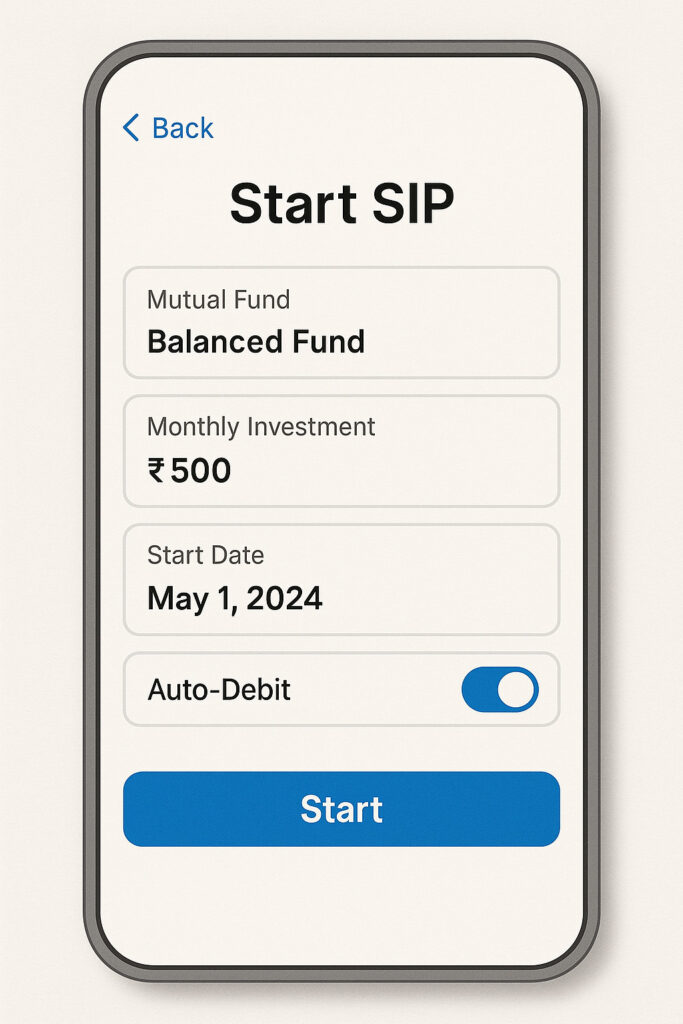

Here’s what I did to start SIP with ₹500:

- Opened the Groww app (you can also try Zerodha, Paytm Money, Kuvera, etc.)

- Completed KYC (PAN, Aadhaar, bank link)

- Searched for a Balanced Mutual Fund

- Hit “Start SIP”

- Selected ₹500/month

- Enabled auto-debit → Done.

In 10 minutes, I had officially started SIP with ₹500 — and felt like I just unlocked a new level of adulting.

🤯 Doubts That Almost Stopped Me

Let’s be real. I had fears. And maybe you do too.

❓ “Is ₹500 even worth it?”

Yes. When you start SIP with ₹500, you’re not chasing money — you’re building a wealth habit.

❓ “What if I lose money?”

In the short term? Maybe.

But SIP is built for long-term — and starting SIP with ₹500 is low risk for learning.

❓ “Should I wait till I have ₹5,000/month?”

No. Waiting is expensive. When you start SIP with ₹500 now, you’re using the most powerful asset: time.

🧮 The Power of ₹500 Compounding

Let’s do some quick math.

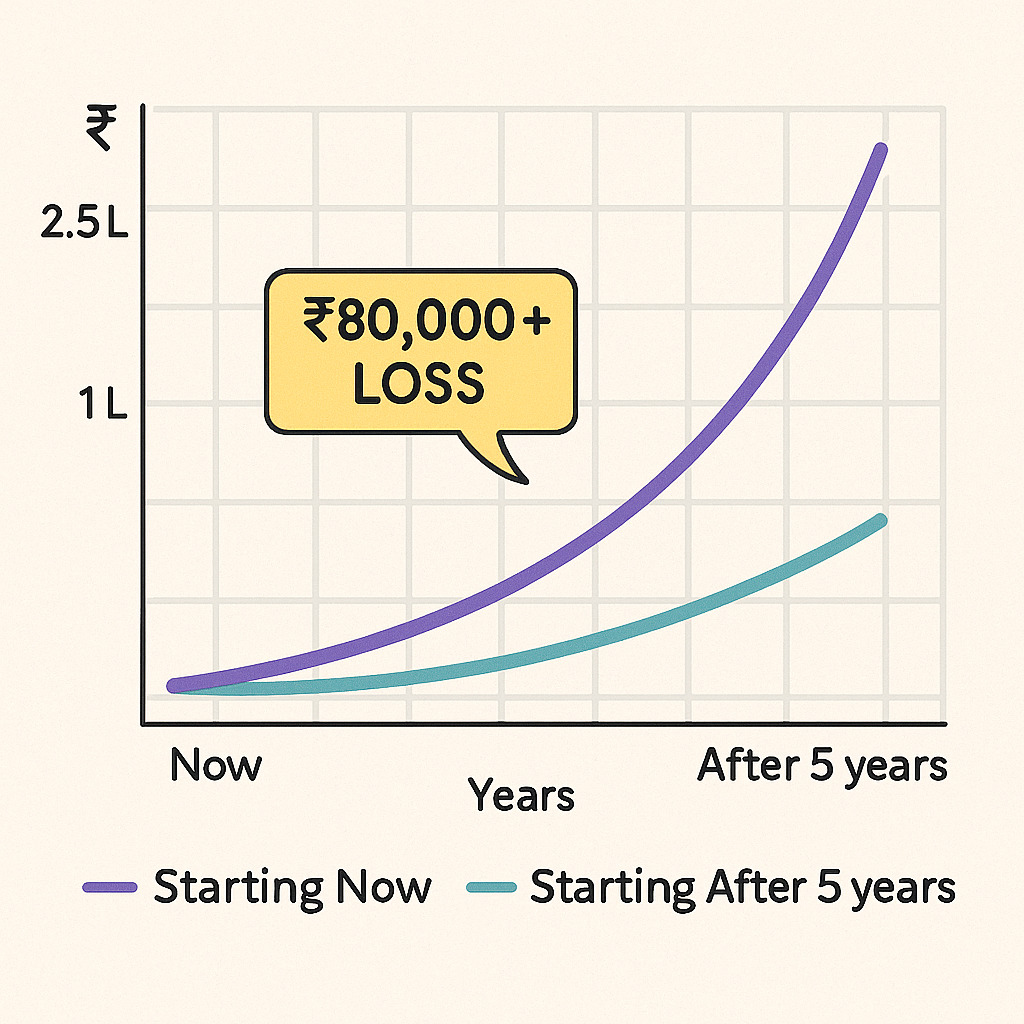

🔢 Scenario 1: ₹500/month SIP for 15 years @ 12%

➡️ You invest: ₹90,000

➡️ You get: ₹2.5+ lakh

➡️ You started SIP with ₹500… and built wealth without stress.

🔢 Scenario 2: Wait 5 years, then start SIP with ₹500

➡️ You lose ₹80,000+ in returns.

Moral? Start SIP with ₹500 now. Small steps > big delays.

📋 How I Track My SIPs Like a Pro

In the beginning, I’d forget dates, skip months, and feel lost.

Now, I use a system that helps me stay consistent with my ₹500 SIP:

✅ My Setup to Track SIP:

- A Google Sheet (SIP name, amount, start date, value)

- Monthly reminders

- Quarterly review — not daily checking

📌 Want my exact setup?

Grab the ₹500 Beginner Budget Toolkit — includes SIP tracker + budget planner.

🧩 Which Mutual Fund Did I Pick?

I didn’t chase high returns. I picked safety to start SIP with ₹500 confidently.

Here’s what I looked for:

- ⭐ Consistent 5-year performance

- 💼 Balanced Fund (Equity + Debt)

- 🛡️ Low risk rating

- 💬 Reviews from other beginners

📌 External Link: Check mutual fund rankings on Groww

📍 Mistakes I Made (So You Don’t)

Before I started SIP with ₹500, I made a few rookie mistakes:

- Delayed for months, waiting for the “perfect time”

- Tried to time the market

- Panicked during small dips and nearly cancelled

Now I know: Start SIP with ₹500. Stick to it. Don’t overthink it.

“Don’t time the market. Spend time in the market.”

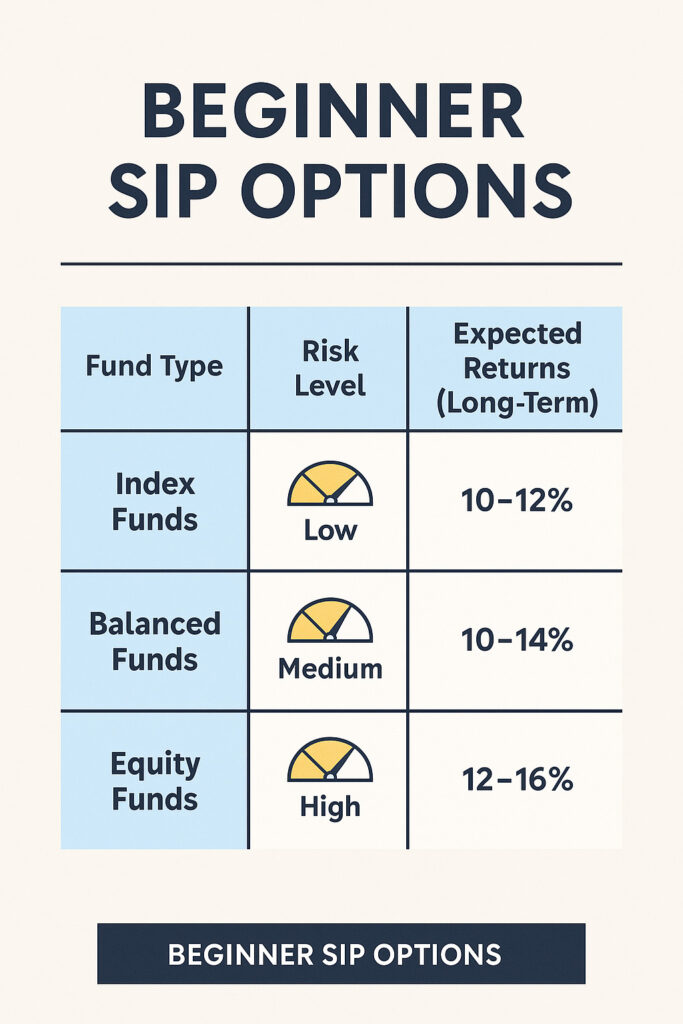

📊 Beginner SIP Options You Can Explore

| Fund Type | Risk Level | Ideal For | Expected Returns |

|---|---|---|---|

| Index Funds | Low | Long-term savers | 10–12% |

| Balanced Funds | Medium | Beginners | 10–14% |

| Equity Funds | High | Aggressive players | 12–16% |

No matter which you choose, remember — start SIP with ₹500 and build discipline before chasing big wins.

🙋♀️ FAQs – Start SIP with ₹500

Q1: Can I really start SIP with ₹500 only?

➡️ Yes, ₹500 is the minimum for most funds. Some start from ₹100.

Q2: Which app should I use?

➡️ Groww, Paytm Money, Kuvera, Zerodha Coin — all are beginner-friendly to start SIP with ₹500.

Q3: What if I miss a month?

➡️ No penalty. Just no investment that month.

Q4: Is SIP better than FD or RD?

➡️ For long-term wealth — yes. But FD/RD are great for short-term or emergency savings.

📌 Related Read: [SIP vs FD vs RD – What I Found Out as a Beginner]

Q5: Can I stop SIP anytime?

➡️ Yes. You can pause, stop, or increase it anytime.

🏁 Final Thoughts: Start Small, Win Big

You don’t need ₹50,000 or a finance degree to start investing.

You just need to start SIP with ₹500 and build from there.

If you’re thinking:

“₹500 is too small to matter”

Let me tell you — it’s not.

Because that ₹500 is your first win.

Your first step.

And the beginning of something way bigger.

🎁 Want to Start Smarter?

Download my free ₹500 Budget Toolkit — the exact tools I used when I decided to start SIP with ₹500.

It includes:

- SIP Tracker

- Budget Planner

- Monthly Goals Sheet

👉 [Grab it here — and start investing like a boss]